In recent months, there has been a noticeable shift in how U.S. Customs and Border Protection (CBP) is handling Requests for Information (CF‑28) and Notices of Action (CF‑29) in the Section 232 and IEEPA tariff context. Importers, brokers, and in‑house counsel should expect more direct CF‑29s proposing duty increases, with less reliance on CF‑28s as an initial information‑gathering step.

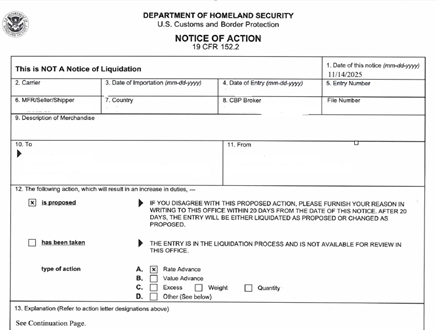

Under 19 U.S.C. 1500 and 1401a, CBP is responsible for appraising merchandise, determining tariff classification, and fixing the rate and final amount of duty owed. When invoices and supporting documentation are not sufficient for appraisement or classification, including to substantiate trade agreement claims, preference treatment, or special provisions, CBP may issue a CF‑28 requesting more information from importers, exporters, producers, or their agents. A CF‑29, by contrast, is a formal notice that CBP intends to change the rate or amount of duty, deny claimed benefits, or liquidate the entry differently—often resulting in additional duties and potential penalty exposure if not addressed promptly.

Shift from CF‑28s to direct CF‑29s

Recently, instead of starting with routine CF‑28s, CBP has increasingly moved directly to proposed CF‑29s where it believes additional duties are owed under 19 C.F.R. § 152.2. This regulation allows CBP to bypass the CF‑28 phase when it determines that the declared value or rate of duty is too low and the resulting increase in duties exceeds $15, a threshold easily met in today’s high‑tariff environment, especially for China‑origin goods subject to Section 232 and related IEEPA measures.

In one recent week, our office received six CF‑29s across four clients, all involving asserted increases in duties under these authorities. The volume, posture, and revenue‑protective framing of these CF‑29s suggest that CBP is now using CF‑29s as an affirmative enforcement and revenue‑protection tool in high‑tariff scenarios, rather than treating CF‑28s as the default preliminary fact‑finding step. For importers, this means less lead time to assemble documents, map supply chains, and frame legal positions before facing proposed duty increases and potential enforcement.

Focus on IEEPA tariffs and derivative steel/aluminum

The recent CF‑29s share a common theme: they target entries where importers relied on exemptions or duty‑mitigation strategies during periods of elevated IEEPA and Section 232 tariff rates. During the height of the China IEEPA tariffs—when the reciprocal tariff rate briefly reached 125% before being reduced to 10% for a defined period—relatively modest disputes over classification or valuation could generate very large duty deltas.

CBP now appears to be revisiting those entries with particular emphasis on whether claimed exemptions and duty‑reducing strategies—such as value‑of‑U.S.‑content deductions, first sale for export, or other special provisions—were properly supported. Beyond IEEPA‑based tariffs, CBP is scrutinizing declared values and exemption claims for Section 232 steel and aluminum derivative articles. Entries where importers split steel/aluminum and non‑steel components into separate lines are drawing attention, especially when that structure lowered the effective duty burden on the steel or derivative component. This has direct implications for importers that structured entries to isolate non‑steel content in mixed‑material products.

Emerging patterns and tighter deadlines

Several patterns emerge across the CF‑29s received. First, CBP is targeting entries with claimed exemptions—such as in‑transit exceptions or value‑content breakouts—during periods of sharply elevated tariff rates, particularly when the same importer has multiple affected entries. Second, entries with line splits between steel/aluminum and non‑steel content in derivative products appear to be a clear focus, reflecting CBP’s concern that tariff‑bearing components may be understated or misallocated.

A particularly concerning trend is the tightening of response deadlines and reduced willingness to grant extensions. Where extensions were previously often available with reasonable justification, they now appear less likely. In the six recent CF‑29s described above, only one extension was granted, and only after escalation within the Center of Excellence and Expertise and a fairness‑based argument. This shift increases pressure on importers and counsel to front‑load fact development, documentation gathering, and internal reviews as soon as a CF‑29 is issued—and to audit vulnerable entries proactively, even before a CF‑28 or CF‑29 arrives, to ensure defensible support exists for claimed exemptions and valuation or classification positions.

What CBP appears to be looking for

The current wave of CF‑29s offers important insight into CBP’s enforcement priorities in the Section 232 and IEEPA context. To protect the revenue, CBP is focusing on entries that claimed exemptions or duty‑mitigating treatments at the time of entry during periods of especially high tariff exposure. When an importer has multiple such entries, CBP appears more inclined to treat the pattern as a potential systemic issue, rather than a one‑off mistake.

For counsel, that raises dual strategic questions: how to respond effectively to the specific CF‑29s in front of them, and whether to consider a prior disclosure or other remedial strategy to manage broader exposure across similarly situated entries. Practitioners advising on Section 232 and IEEPA risk should be prepared to address both levels—entry‑specific defenses and portfolio‑wide strategy—balancing revenue risk, penalty exposure, and operational realities.

Clarified “non‑steel” and “non‑aluminum” guidance

One of the more challenging aspects of the current enforcement environment is the apparent existence of internal CBP guidance on what qualifies as “non‑steel” or “non‑aluminum” content in derivative products. The Base Metals Center of Excellence and Expertise has used consistent language when describing what CBP considers to be non‑steel or non‑aluminum content in CF‑29s and related communications.

In practice, CBP is stating that “non‑steel content” does not include fabrication, machining, labor, or similar processing costs associated with producing a steel or aluminum article, and does not include the manufacturer’s profit. In other words, for Section 232 purposes, the steel or aluminum content must be declared at its full “loaded” cost. That position has been articulated in emails involving senior Center personnel and is appearing in CF‑29s addressing Section 232 derivative articles.

Practical next steps for importers

Given these trends, importers facing Section 232 and IEEPA exposure should consider:

- Proactively reviewing entries that claimed exemptions, first sale, U.S.‑content deductions, or line‑splitting strategies during periods of elevated tariff rates.

- Ensuring that documentation is organized and readily available to support valuation, classification, and exemption claims before a CF‑29 arrives.

- Coordinating with customs counsel on whether a targeted prior disclosure or other remedial strategy is appropriate where patterns of risk are identified.

Our Customs and Trade team is actively assisting importers in navigating this wave of CF‑29s and related enforcement activity. If you have received a CF‑29 tied to Section 232 or IEEPA tariffs—or have questions about how your entry strategies may be viewed by CBP in this environment—please contact us.